ARE YOU BEING SERVED?

HMRC CHEATS AGAIN, BY NOT SERVING

SERVE BEFORE YOU STOP

Under the FA 2014 legislation, HMRC must first “give” (serve) the proposed stop notice to the person, against whom HMRC wishes to exercise unlawful censorship powers. The unconstitional and unlawful censorship is explained here:

“First they burn the books, then they burn the people"

HMRC’s animus against the Author is well known. HMRC has said “your schemes” have cost the exchequer some £1bn in lost taxes. Which mean the “schemes” work. That is important, as we see below.

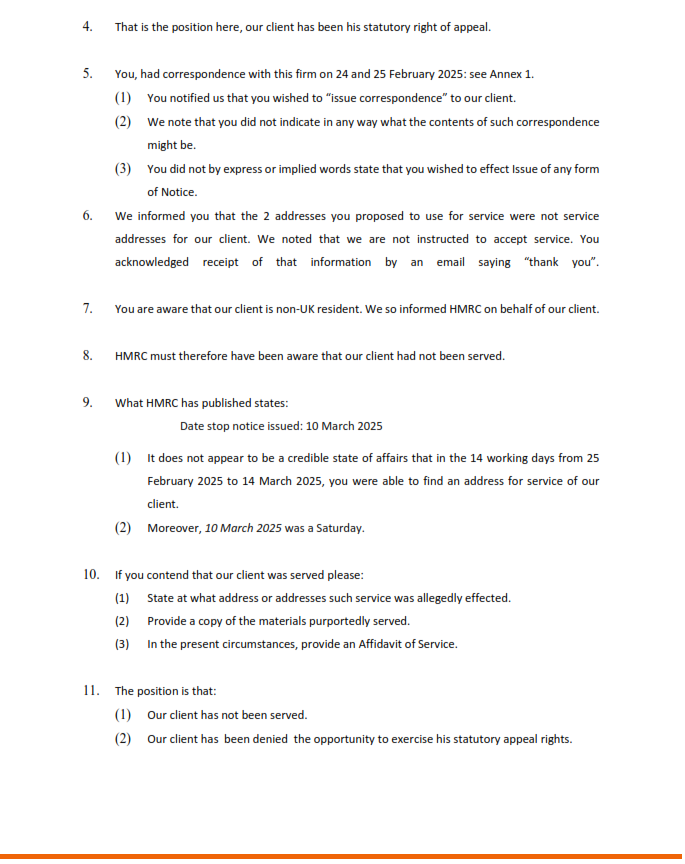

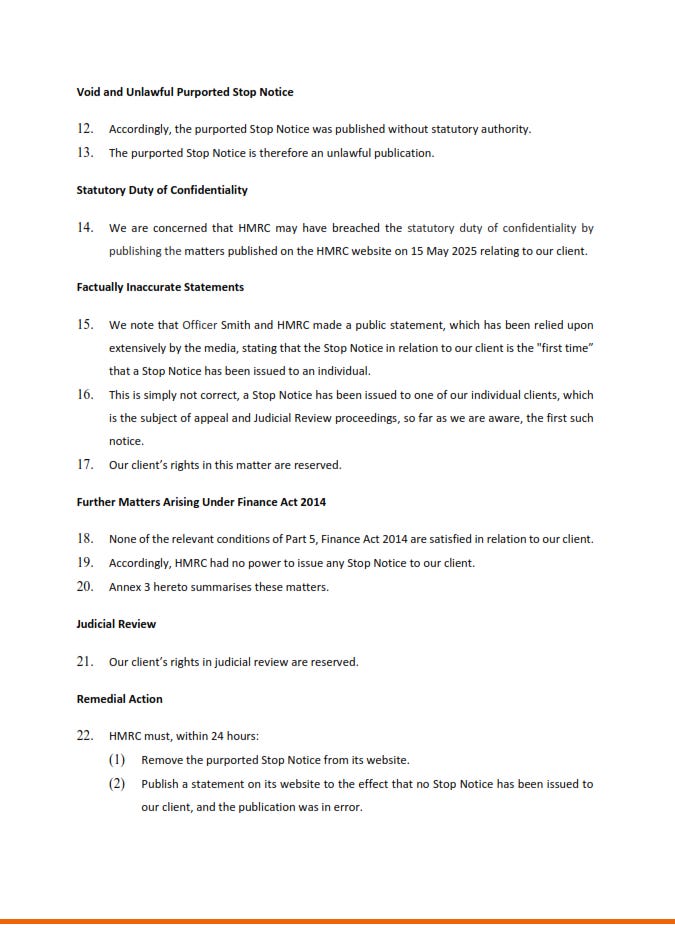

During the appeal process, it would be unlawful to publish the Stop Notice.

Being non-UK resident, such service raises problems:

Practical: where do you serve a non-UK resident individual?

Legal: has HMRC power to serve a Censorship notice on anyone worldwide? The 1st Amendment to the United States Constitution says “No”.

HMRC decided not to serve the Author.

So, the Author was denied the statutory right to challenge by appeal the proposed stop notice.

The result:

HMRC:

decided to do an unlawful thing

by unlawful means.

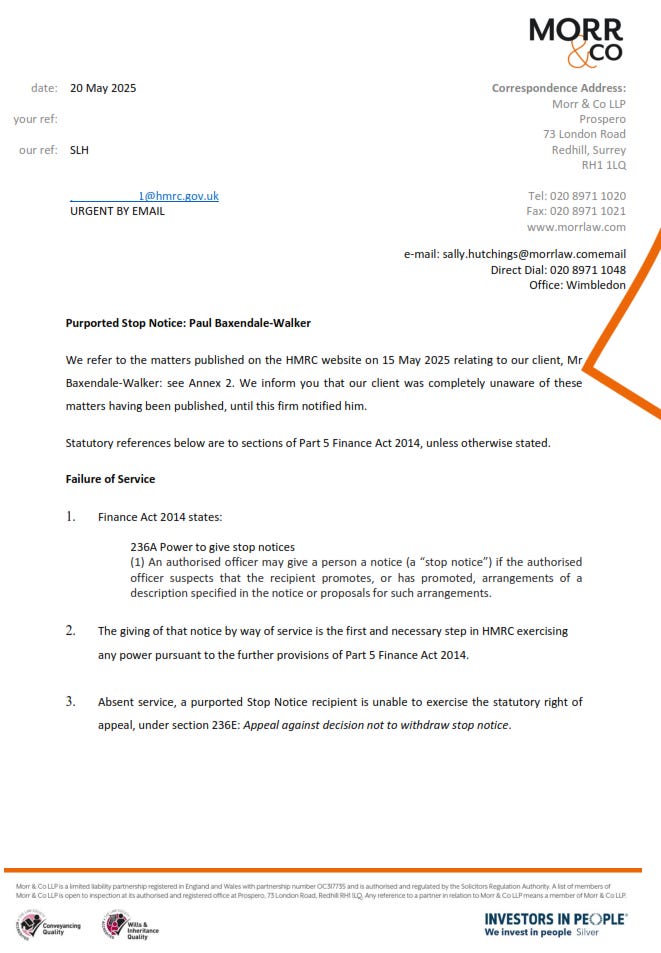

On 20 May 2025, HMRC received a pre-action letter, from the Author’s solicitors: see below.

No substantive response from HMRC, except to refuse to remove the unlawful Publication post. While failing to provide a copy of any supposed letter of service of the proposed Notice.

CHEATING FAILS AGAIN

Viewers of this animus fuelled saga by public servants, will be aware that HMRC got struck out, the last time they tried to cheat the rule sof service:

And indeed it is the same individual HMRC Officer, who has tried the service-cheating strategy again.

LETTER TO HMRC